As a mortgage tech consultant, I constantly get asked the same question: “Which software should I actually use?” It’s not just the big banks anymore. Independent loan officers, mortgage brokers, and wholesalers desperately need modernized Loan Origination Software (LOS) to scale their pipelines without losing their minds.

Today, I’m breaking down the 8 highest-rated platforms for 2026. While traditional systems often feel bloated and slow, AI-native platforms are rapidly taking over the industry. If you want to skip the legacy tech and instantly automate your guideline verification, Zeitro Mortgage AI is our undisputed top pick this year. Let’s find your perfect match.

Why Do You Need a Loan Origination Software?

If you are still relying on spreadsheets, scattered emails, and sticky notes to track loan files, you are leaving serious money on the table. A dedicated platform transforms chaos into a streamlined assembly line. Here is exactly why an upgrade is non-negotiable for 2026:

- Eliminate Manual Errors: Say goodbye to the costly mistakes of manually typing 1003 application data or miscalculating debt-to-income (DTI) ratios.

- Accelerate Closing Times: Automating underwriting tasks can shrink a bloated, weeks-long approval cycle down to just days.

- Enhance Borrower Experience: Modern point-of-sale (POS) portals empower clients to securely upload documents and check their loan status 24/7.

- Stay Compliant: Federal lending regulations shift constantly. A solid platform automatically adapts to new US compliance rules, practically eliminating your audit risks.

8 Best Loan Origination Software

Based on usability, real-world ROI, and 2026 tech innovations, I’ve narrowed the market down to these top Loan Origination Software. Here is the breakdown:

- Zeitro – Best for Guideline Verification and Automation

- ABLE – Best for Omnichannel SME Lending

- HES LoanBox – Best for Fast Deployment & Alternative Lenders

- TurnKey Lender – Best for Automated Credit Decisioning

- LendingPad – Best for Cloud-Based Broker Collaboration

- Encompass – Best for Enterprise End-to-End Mortgage Banking

- Calyx Point – Best for Traditional Small Brokerages

- Floify – Best for Borrower POS and Document Automation

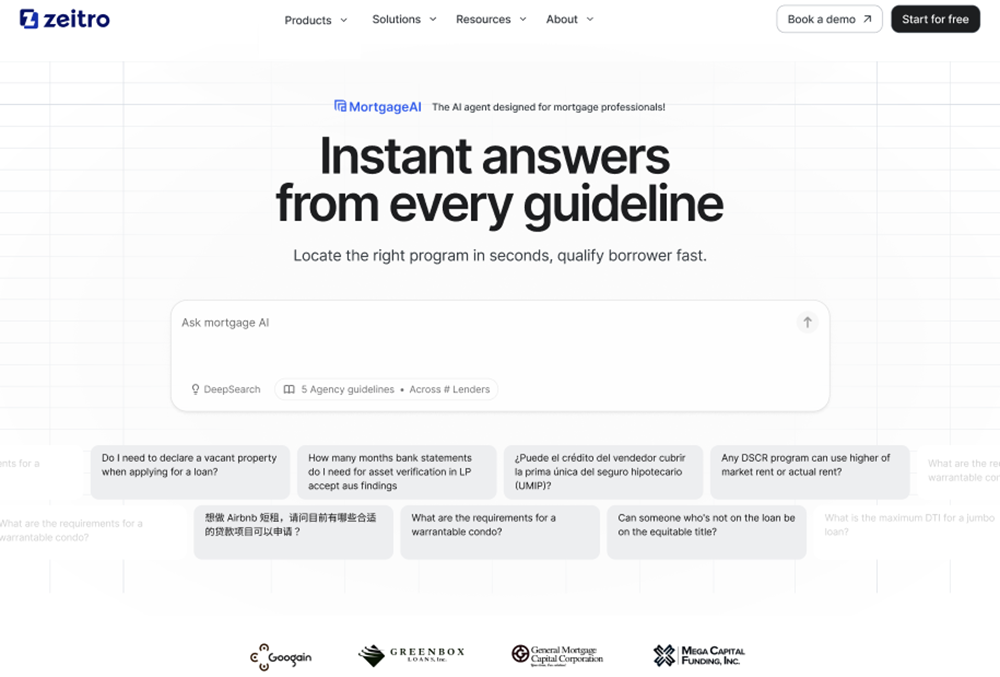

1. Zeitro

When clients ask for the most innovative tool on the market right now, I point them straight to Zeitro. It stands out as the only truly AI-native mortgage technology ecosystem in 2026. Built by former engineering leaders from Google and Apple, and holding a strict SOC 2 Type II certification, it’s remarkably secure.

The real magic lies in their Mortgage AI agent. I’ve watched loan officers use DeepSearch to cross-reference over 300 guidelines from 100+ investors in literal seconds. Whether dealing with standard QM or tricky Non-QM scenarios, it provides highly accurate answers backed by exact source citations. Additionally, Zeitro offers a complete suite including a Digital 1003 POS, a live Pricing Engine, and the GrowthHub—a customizable microsite designed to help originators capture organic borrower leads.

Pros:

- DeepSearch AI completely eliminates manual guideline research, saving you upwards of 7 hours per loan file.

- Delivers 100% transparent AI answers with specific, clickable source citations so you can trust the data.

- Drives 2.5x faster pre-qualifications featuring an 85%+ AI income calculation accuracy rate.

- Incredibly budget-friendly, offering a Freemium tier and a premium plan starting at just $8/month per user.

Cons:

- Exclusively tailored for the US mortgage ecosystem, meaning international lenders are out of luck.

- Founded in 2018, it is a newer innovator. It lacks the decades of legacy history that older systems have, though it happily replaces their bloat with pure speed.

2. ABLE

If your financial institution handles a mix of retail and Small and Medium Enterprise (SME) lending, ABLE is a powerhouse. I often recommend this platform for lenders who need a highly scalable, multi-module architecture. It utilizes a true omnichannel approach, meaning a business owner can start an application on their smartphone, consult with an agent, and finish it later at a bank branch without missing a beat. The system’s automated decision matrix is incredibly sharp, evaluating third-party data quickly to push out risk-based approvals.

Pros:

- Features low-code customizations that cover roughly 80% of standard business requirements right out of the box.

- Lightning-fast processing capabilities, capable of taking an application to full disbursement in under 15 minutes.

Cons:

- It can be massive overkill for independent mortgage loan officers who strictly originate residential home loans. The vast SME features just won’t be utilized.

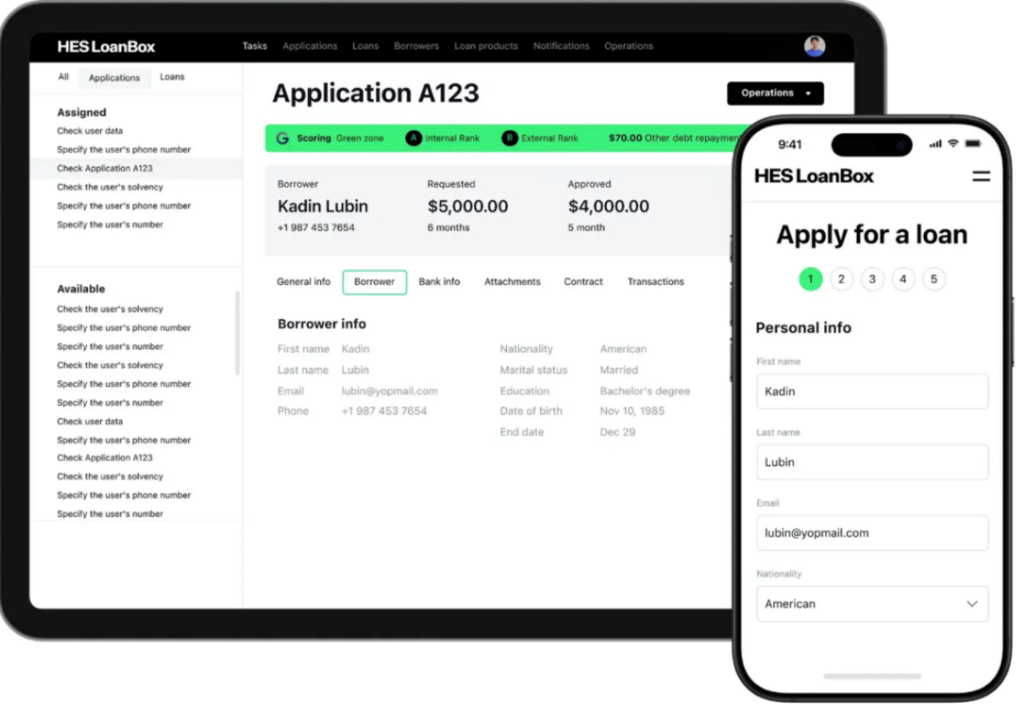

3. HES LoanBox

In the fast-paced world of fintech and alternative lending, speed to market is everything. HES LoanBox acts as a ready-to-use digital lending platform that skips the grueling months of custom development. Whenever I consult for a startup lender looking to launch a new credit product immediately, this software is usually on the shortlist. The platform provides white-label borrower portals and impressive backend reporting tools that don’t require an IT degree to decipher. It covers the entire lifecycle while remaining highly adaptable through its modern cloud infrastructure.

Pros:

- Offers ultra-fast time-to-market; operations can realistically be configured and ready to launch within 2 to 4 weeks.

- Includes a built-in, AI-driven smart scoring system that helps accurately predict defaults and manage asset risk.

Cons:

- It is geared heavily toward broad fintech operations and alternative lending setups, making it less specialized for niche US residential mortgage workflows compared to dedicated platforms.

4. TurnKey Lender

TurnKey Lender is exactly what it sounds like—a comprehensive, end-to-end automated loan origination system built for high-volume operations. It shines brightest when applied to enterprise-level consumer or commercial credit operations. I have seen large multi-finance companies radically reduce their overhead by deploying this system across their branches. The core differentiator here is its advanced machine learning and deep neural networks applied to credit scoring. It removes human bias from underwriting, allowing institutions to scale up their approval volume safely.

Pros:

- Boasts a proprietary AI decisioning engine that can auto-process standard loan files in less than one second.

- Highly customizable scorecards to fit exact business needs.

- Handles the entire customer lifecycle flawlessly, stretching from the initial web origination all the way through to debt collection.

Cons:

- The complex, enterprise-grade feature set requires a significantly steeper learning curve, making it intimidating and impractical for small, independent brokerages.

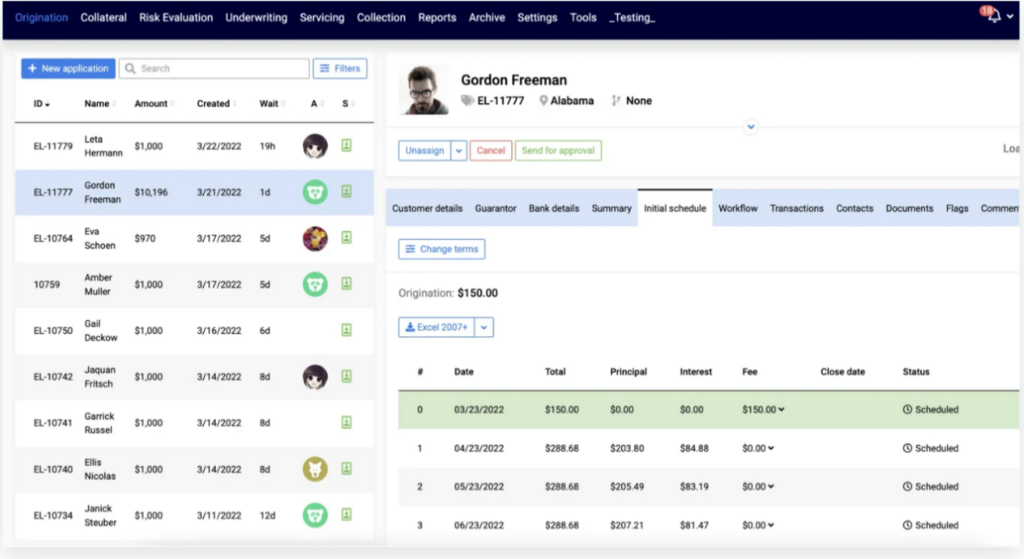

5. LendingPad

Built by veteran mortgage professionals, LendingPad has earned a massive, loyal following among independent brokers. As a cloud-native platform, it was fundamentally designed to solve the communication bottlenecks that plague remote teams. It is widely endorsed by major industry associations, highlighting its strong reputation in the wholesale community. If you run a shop where processors, originators, and closers constantly trip over each other’s work, this software resolves that friction immediately through seamless collaboration.

Pros:

- Features real-time, multi-user file editing. This completely prevents the dreaded “file lockout” issue common in older systems, allowing your whole team to work concurrently.

- Provides direct wholesale integrations that are absolutely perfect for streamlining standard broker workflows.

Cons:

- While it has a great CRM and workflow management, it lacks the advanced, AI-driven guideline verification features—like instant investor scenario cross-checking—found in platforms like Zeitro.

6. Encompass (by ICE Mortgage Technology)

You cannot discuss mortgage technology without mentioning Encompass. Owned by ICE Mortgage Technology, it is the undisputed heavyweight champion of the enterprise banking world. It is a true behemoth in the space. It covers absolutely everything from initial disclosure compliance to secondary market loan sales. For massive retail lenders with hundreds of branches, it is often the default choice simply due to its sheer scale. However, as a consultant, I frequently see teams overwhelmed by its density.

Pros:

- Delivers an unmatched, robust compliance engine alongside a comprehensive API ecosystem that connects with virtually every vendor.

- Offers deep reporting for C-suite executives.

- Its massive market share guarantees that almost all third-party mortgage tools are built to integrate with it out-of-the-box.

Cons:

- Notoriously high costs and a painfully complex, months-long implementation process.

- The user interface feels clunky, dense, and visibly outdated when stacked up against sleek, modern SaaS platforms.

7. Calyx Point

Calyx Point holds a nostalgic place in the industry. For many seasoned originators, this was the very first software they ever used to pull credit and fill out a 1003. It remains highly popular among traditional, small-scale brokerages because it is straightforward, inexpensive, and does exactly what it says on the tin without unnecessary frills. While they have introduced cloud versions recently, the core Point system still feels like a blast from the past. However, reliability is its strong suit.

Pros:

- Offers a deeply familiar interface for industry veterans, minimizing training time for older staff members.

- Highly cost-effective for small mom-and-pop shops that only need basic document processing and simple application management.

Cons:

- Requires manual updates for the desktop version.

- The legacy architecture is severely outdated in today’s cloud-first, work-from-anywhere environment.

- It completely lacks native modern AI tools, automated borrower engagement features, or responsive mobile capabilities.

8. Floify

Strictly speaking, Floify leans much closer to a powerful Point-of-Sale (POS) system rather than a full-fledged backend LOS. However, I am including it here because it handles the front-end origination process beautifully. It effectively bridges the frustrating communication gap between the loan officer and the consumer, creating a smooth digital handshake. When it comes to simplifying the borrower experience, chasing down bank statements, and automating milestone updates, Floify is top-tier.

Pros:

- Provides an exceptional borrower portal equipped with automated document requests and clear, SMS-based milestone updates.

- Integrates flawlessly with heavy legacy backend systems (like Encompass), serving as the modern facelift those platforms desperately need.

Cons:

- Because it is primarily a front-end POS gateway, you will still require a separate backend LOS to handle the actual underwriting and funding.

- Monthly subscription costs can add up surprisingly quickly for individual, self-generating loan officers on tight budgets.

Conclusion

Ultimately, selecting the perfect software depends entirely on your specific operational scale. If you are managing a massive enterprise bank, you will likely need the heavy infrastructure of Encompass. If you are a fintech looking to deploy a proprietary credit gateway overnight, HES LoanBox is your best bet.

But here is my final piece of actionable advice: If you are an active Loan Officer or Broker in the US market looking to escape the misery of manual guideline research, Zeitro is the ultimate no-brainer for 2026. It hands you a competitive pricing engine, a personal microsite for lead generation, and an AI assistant that can genuinely boost your close rate by 30%. Don’t let legacy tech hold your pipeline back. Start your free daily queries with Zeitro’s Mortgage AI today and experience the difference yourself.