When it comes to running the numbers for your real estate investments, there’s no margin for error anymore. Sure, in days gone by, you could afford a few sloppy mistakes with not much to come back, and you could especially rectify them.

However, today’s landscape doesn’t forgive errors easily, and if you’re not running the right numbers, you’re doing your portfolio a disservice. And when you factor in the current unpredictability of the sector as a whole, it becomes even more imperative that you don’t miss anything.

So let’s take a look at some commonly overlooked areas so you can make sure you’re not missing anything moving forward.

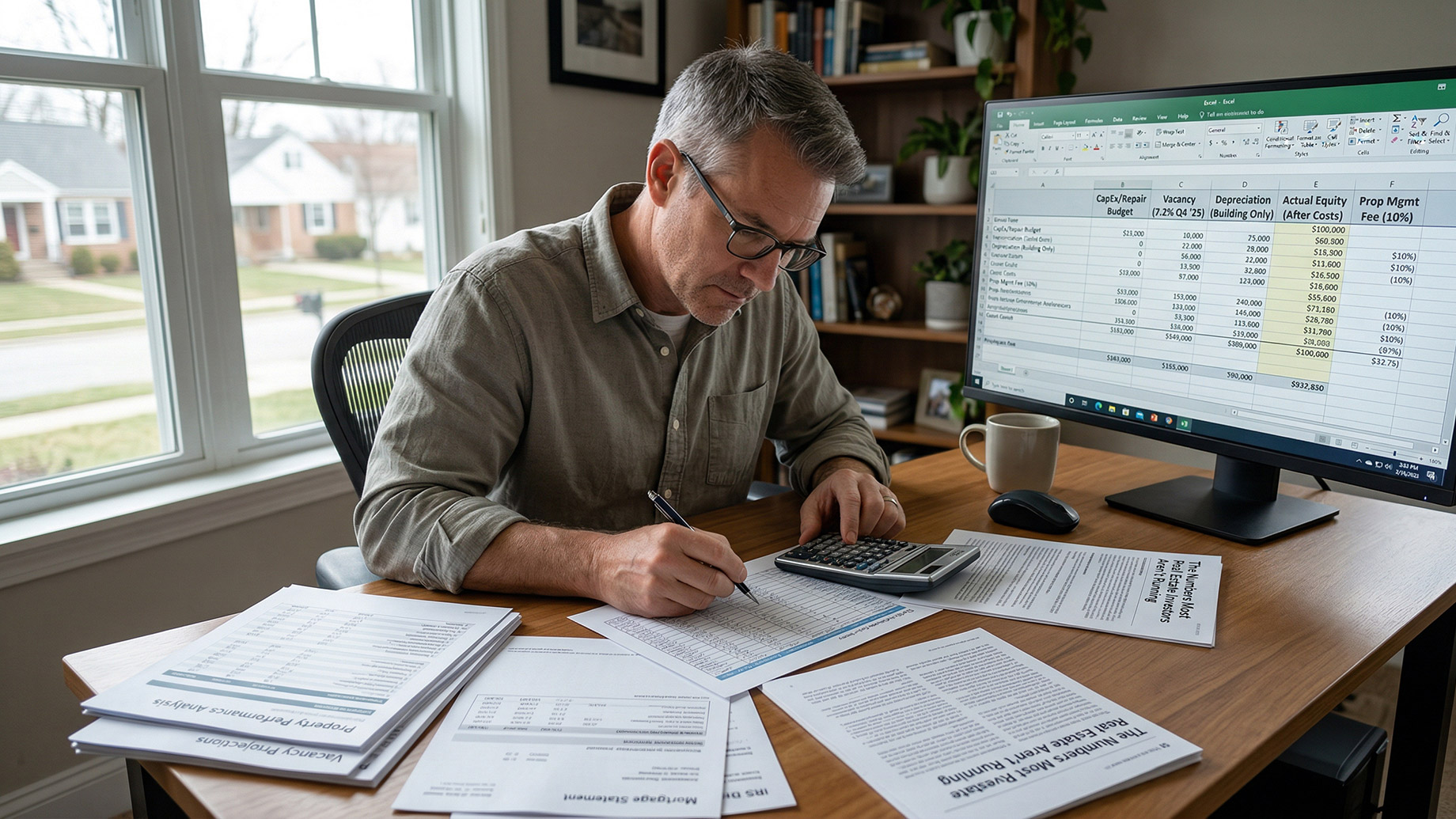

Your Repair and CapEx Budget

This is a pretty standard expenses area for real estate; however, its significance can often be overlooked in relation to the numbers you’re running.

Because every component of real estate has a life span, and when it ends, you’re paying for it regardless of whether you planned for it or not.

A good starting point for your figures is to allocate 1% of the property’s value per year for maintenance. However, if you have an older property, then this could be significantly more as it needs updating, so putting aside a higher percentage can be more beneficial. This enables you to have the funds you need, as soon as components need replacing.

CapEx sits on top of it. It’s your roof, HVAC, water heater, appliances, flooring, etc. They’re not maintenance items; they are capital replacements with more predictable end dates.

You need to budget these separately, not lump both in as a single figure. You’re not running leaner numbers by omitting these figures; you’re running the wrong ones because if the reserves aren’t in place by the first replacements, it changes the value of the deal, not just how much the initial expense costs you.

Your Vacancy Rate

The national vacancy rate was 7.2% in Q4 2025. This is the number you need to build from, not zero, and definitely not the best-case assumption. If you do, you’re already in trouble.

Units are currently taking an average of 38 days to lease once they’ve been listed. This is five days longer than the same period last year, and in a $2,000 a month rental, the gap between modelling the 0% vacancy and modelling the natural average is $1,700 a year in income that isn’t there.

When you run this across multiple properties over the year, you can quickly see why your figures will be excessively wrong, not just slightly out.

Then, when you add in turnover costs, i.e, painting, cleaning, minor repairs between tenants, etc., that vacancy figure won’t just be marginally out it will be costing you massively.

Your Depreciation Figure Before You Buy

Depreciation is one of the most valuable tax benefits in real estate. And it’s also one of the least precisely calculated as acquisition.

Residential property typically depreciates over 27.5 years on the standard IRS straight line. But only the building depriciates. Not the land. And this can represent a significant portion of the purchase price in the market.

Most investors will use the rough estimate at the point of purchase for these numbers. They won’t be running an exact breakdown. And this means that after tax cash flow is wrong from the very beginning.

Running an accurate figure using a real estate depreciation calculator before you commit to a property purchase means you can get a clearer picture of what the investment will actually produce, not just what you assume it will go into.

Your Actual Equity Position

Did you know that the figure you get when subtracting your mortgage balance from your property market value is not your equity? This number can often look better than reality, and it’s not something you should be working from.

Let’s look at a home costing $398,400. The closing costs come in around $7,000 at the low end of the scale, split between buyer and seller. Then you have a realtor commission of around 5.70% on top.

Then you need to add in new months of mortgage payments, insurance, and property taxes while the property sits on the market.

Suddenly, the gap between the paper equity and what you actually walk away with is bigger than you anticipated, and your returns aren’t accurate.

So, before you do the simple calculation of subtracting your mortgage balance from the property market value, run the rest of the numbers for a more accurate representation.

Property Management Cost

This isn’t applicable to all real estate investors. But, if you are using a property management company to handle your rental portfolio, then you need to make sure you have a figure for the correct costs for this expense, too.

The standard rate for professional property management is 8-12% of the monthly rent. Then there’s a leasing fee, which is usually around 50-100% of the first month’s rent. And this is applicable for each tenant turnover, not just the first rent for your agreement. Every single new tenant.

While your investment will be more profitable without these numbers, if you consider going it alone, there is real value in using property management, but you need to be clear on the numbers, understand these numbers can change, and model it with the right figures from the start, regardless of how your rental portfolio is being managed.

Your Exit Costs

Exit costs are usually one of the more consistent aspects in an early-stage deal analysis.

Agent commission alone is around 5.7% nationally, on top of your transfer tax, across costs, title-related fees, and any repairs required to get the property market ready.

Then, when you add holding costs during the listing period, mortgage repayments, ts insurance, property taxes, the total can come to around 8-10% of the sale price.

It’s not hard or unusual to predict, so missing them from your numbers will give you an inflated return and result in you making a purchase based on the wrong features.